“Modern consumers demand convenience, security, and flexibility when paying for their goods and services, and like it or not; legal clients are no different.” The American Bar Association (ABA) emphasizes that offering diverse payment options is critical for meeting client expectations and enhancing their experience.

Furthermore, the ABA admonishes, “[i]f your firm fails to provide the payment options that modern clients want, you risk falling short of client expectations. Poor client experience can snowball into a whole host of problems for your firm, including poor client retention, little to no client referrals, and ultimately hurting your law firm’s profitability.”

The legal field is a sector of life that provides necessary services and expertise that is not always readily able to be reduced, like your neighborhood grocery store’s discount sale. So, what do attorneys do in these situations? What is the best strategy for providing necessary services to the public and ensuring equal access to legal services without harming your practice? Establishing an alternative payment plan structure may be the answer for you and your clients.

Why Your Firm Needs Multiple Payment Methods.

Having multiple payment methods available for your firm is essential for several compelling reasons:

- Provide convenience to your clients. Different clients have different preferences when it comes to making payments. Offering multiple payment methods ensures that you accommodate a broader range of clients, making it more convenient for them to settle their bills. Whether they prefer credit cards, bank transfers, checks, or digital payment platforms like PayPal or Venmo, having various options enhances accessibility.

- Receive payment faster. Diversifying payment methods can lead to faster and more reliable cash flow for your firm. Clients with flexible payment options are more likely to pay promptly, reducing the likelihood of delayed or missed payments.

- Improved cash flow management. Relying on a single payment method can expose your firm to risks, such as system outages or issues with a specific payment provider. Multiple payment methods minimize the impact of such disruptions, ensuring your firm’s financial operations remain stable.

Having multiple payment plan options is a prudent strategy that aligns with modern client expectations and the changing landscape of financial transactions.

What Is Legal Fee Financing?

Legal fee financing is a financial arrangement in which a third-party entity, often a specialized financing company or lender, provides financial assistance to individuals or businesses to cover their legal expenses. This assistance allows clients to access legal services and representation without paying the total cost of legal fees upfront. Instead, clients can spread the payment over time, typically in installments.

In legal fee financing, the financing entity may charge interest or fees for extending the credit, which can vary depending on the terms of the agreement. The law firm receives the entire payment upfront, while the client can make installments to the third-party creditor.

This approach helps individuals and businesses afford legal services when they might not have the immediate funds to cover legal costs, making it an attractive option for those facing legal issues but lacking the financial resources to address them immediately.

How Are Payment Plans Different from Legal Fee Financing?

Legal fee financing and payment plans are two distinct strategies law firms can employ to facilitate access to legal services for their clients. Legal fee financing involves third-party financiers who cover the entirety or a portion of a client’s legal fees. This arrangement often comes with interest rates and specific repayment terms.

On the other hand, payment plans are agreements directly between the client and the law firm. Clients pay their legal fees over a predetermined period, typically in installments. Choosing this method also provides an opportunity for higher client satisfaction and ratings because offering the payment plan directly gives clients a message of empathy and care.

Choosing between these options hinges on several factors.

- Legal fee financing offers immediate relief to clients but may incur additional costs due to interests.

- Payment plans, conversely, involve no interest but require firms to manage collection and may lead to delayed revenue.

- Both options require clients to make regular and consistent on-time payments based on the payment interval established with the firm or the third-party creditor.

Ultimately, the choice between legal fee financing and payment plans should align with the firm’s long-term growth objectives and client satisfaction.

How to Determine if Alternative Payment Arrangements Are Right for Your Firm

Determining if alternative payment arrangements suit your firm involves carefully assessing various factors to ensure they align with your firm’s goals and client base.

Balancing client accessibility with financial sustainability is paramount. Determine your firm’s and client’s needs. Here are some steps to help you make an informed decision:

- Assess your firm’s financial health and cash flow. Determine if your firm can absorb any potential delays in fee collection that might result from alternative payment arrangements.

- Determine how your firm charges, such as hourly, fixed flat rate, or contingency fee, and see which alternative payment arrangement fits the best.

- Assess which areas of law you primarily focus on and whether those practice areas align with alternative payment models.

- Ensure that any alternative payment arrangements you consider comply with legal and ethical regulations governing your jurisdiction. Consult with legal experts to navigate regulatory complexities.

- Research what payment options your competitors offer and understand market trends to determine whether adopting similar strategies would give you a competitive edge.

- Finally, consider implementing small-scale pilot programs to test the viability of alternative payment arrangements. Measure the response from clients and assess the impact on your firm’s finances.

The Benefits of Offering Alternative Payment Arrangements

Offering alternative payment arrangements can provide several significant advantages for law firms. Alternative payment arrangements can be especially beneficial when legal matters are complex, time-consuming, or involve substantial legal fees, as they ease the financial burden on clients and enable them to secure legal representation when needed.

These arrangements cater to a diverse client base and enhance the accessibility of legal services, ultimately contributing to the firm’s success. Here are some key advantages:

- Offering payment plans or financing can allow your clients to budget for legal expenses over time, reducing the financial strain of legal matters.

- Alternative payment arrangements can help stabilize your firm’s cash flow. While traditional fees may have irregular payment schedules, alternative methods often result in more predictable revenue streams.

- Having a payment plan option reduces the time your firm will need to spend on collections. This allows you to divert time spent on collections to completing meaningful work that focuses on increasing revenue.

- Different clients have varying financial situations. Alternative arrangements allow you to cater to a broad spectrum of clients, from individuals with modest means to businesses with complex financial structures.

Offering flexibility in payment arrangements demonstrates your commitment to client-centric solutions. This can build a positive reputation in the legal community and among clients.

Implementing Alternative Payment Arrangements

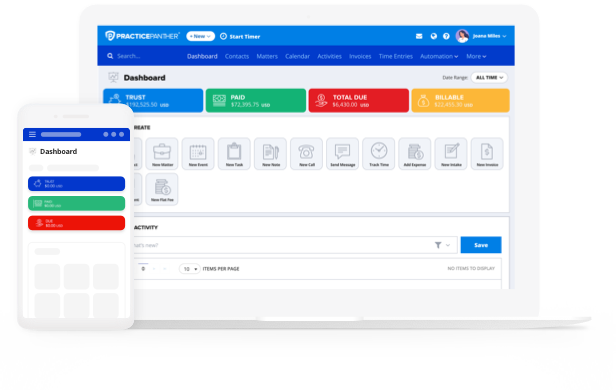

Implementing alternative payment arrangements in your law firm is a strategic move that can make a difference in your law firm’s collection. While we discussed the available payment plan options, their benefits, differences, and overall impact within a legal firm, the most crucial factor to consider is having the right legal billing management software to facilitate different payment collection capabilities.

Utilizing legal software like PracticePanther for this purpose has many benefits. For instance, PracticePanther hosts a billing framework strategically set up to personalize your payment collection options called PantherPayments. Using this billing system, you can:

- Streamline your legal billing process.

- Set up customized automated payment plans to address client needs.

- Track payments and develop reports to ensure proficient cash flow.

- Put the client’s interest first and show them your firm cares about everything concerning them, including their financial peace.

Gain a Competitive Edge

Incorporating alternative payment options can help your firm stand out by offering clients the flexibility they value. These arrangements not only stabilize cash flow but also make legal services more accessible to those who might otherwise struggle to pay upfront. Balancing your clients’ needs with your firm’s financial health is a smart move that fosters trust and builds long-term relationships.

Using a platform like PracticePanther simplifies this process. With features like PantherPayments, you can set up automated payment plans, track payments with ease, and keep your billing process organized — all while maintaining a client-centered approach. Making payments easy and transparent benefits both your firm and your clients.

If you’re ready to see how PracticePanther can support your firm’s goals, sign up for a free trial today, or click below to schedule a demo customized to your firm’s needs.